on the

money

read time 5min

FINANCIAL INCLUSION

ccording to World Bank estimates, about 45% of 882 million adults in Africa do not have access to a bank account. There is no other market where the necessity to remove friction and make financial services and payments more inclusive and accessible is more prevalent than on our own continent.

“If you consider adults who actively use their bank account, then this is likely to constitute a market of around 100 million adults across the continent,” says Sachin Shah, Head: Payments and Receivables, Transaction Banking at Standard Bank Corporate and Investment Banking. “But the moment you expand that to wallets, your target population grows to nearly a billion. That’s a massive leap.” Manufacturers and service providers want to be able to sell their products and services to these customers and unlock the growth potential which exists on the continent. Enabling payments to and from these customers is the catalyst through which this can happen.

Access to Payment Rails

South Africa is unique in the maturity of account payments and card-based solutions, which still form the primary means of payments processing and settlement in the market. The National Payment System Act in South Africa currently excludes non-banks from directly accessing the settlement system, which means that they require a bank sponsor to settle transactions.

This can be illustrated as a central hub of settlement participants radiating outwards to clearing participants, payment services, third-party payment providers and a final ring encapsulating customers, retailers and corporates. The picture looks like a target – and non-financial banking solutions providers will see it as exactly that. They’re currently only able to access the third-outermost ring that the third-party payment providers are regulated into, but they’re aiming for the bull’s-eye.

In most other markets, mobile or wallet payment volumes have overtaken account and card payments, especially as a form of settlement for low value, instant payment transactions. Whereas the principles in many instances are similar to South Africa’s National Payment System Act (78 of 1998), the models have also evolved based on local requirements. Banks including Standard Bank still play a critical role within this value chain – holding the trust accounts which contain 100% of the funds equivalent to the mobile money in circulation. This is the foundation of a partnership which can evolve to so much more.

“With every household in Africa expected to have access to a mobile phone with internet access by 2030 or even sooner, mobile wallets can provide more ubiquity than any other digital financial instrument,” says Shah. “The impact this can have on the digitisation of payments cannot be underestimated.” South Africa’s new interbank digital payment service PayShap is a step in that direction, enabling customers to pay and be paid instantly using a mobile phone number instead of having to share their bank account details.

The Face of Payments

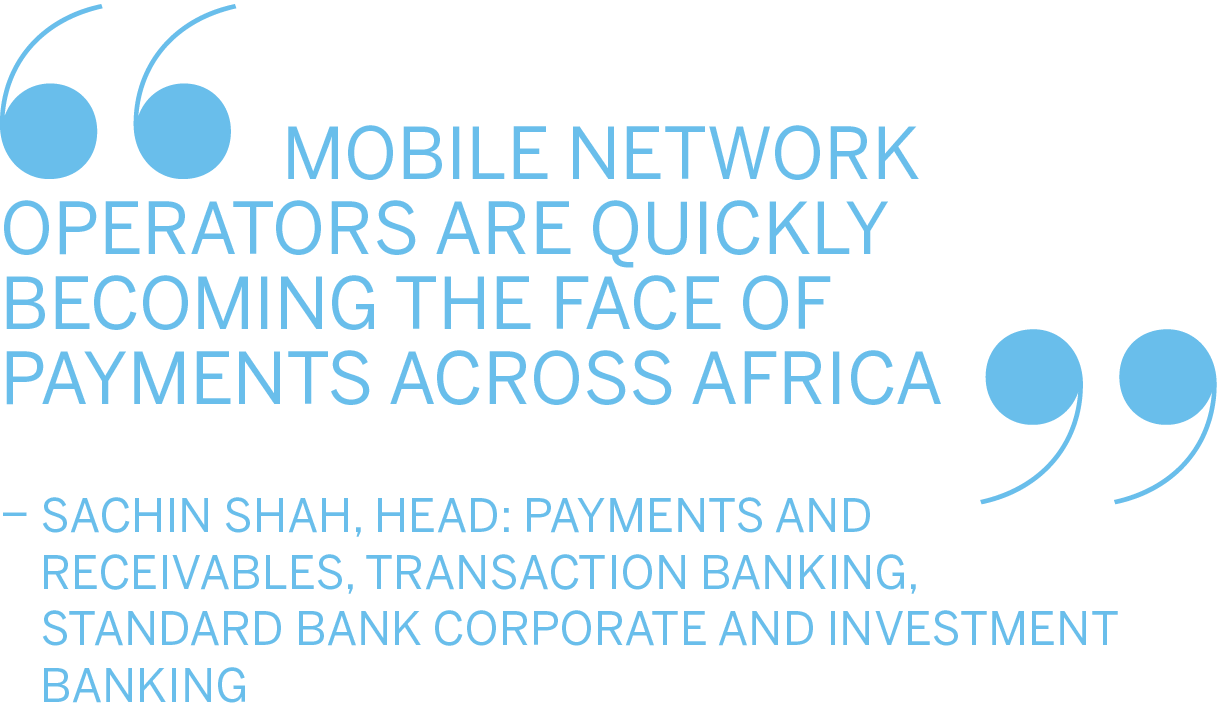

“With the benefit of a vast subscriber base as well as a significant agent base, Mobile Network Operators (MNOs) are quickly becoming the face of payments across Africa” says Shah. “One of their key benefits is also being able to offer last mile access to cash – as cash transactions still constitute a significant percentage of all mobile money transactions”. Their growth potential has not gone unnoticed, with multi-million-dollar investments into the mobile money entities from global giants including Mastercard and Visa.

In South Africa, the retail sector, in turn, is also being rapidly disrupted. What started off as the provision of services like cashback at tills and bill payments is rapidly expanding to money remittances, the opening of bank accounts as well as strategies to offer their own wallets. Through their vast customer base and by leveraging the data that they hold, both the retailers and telcos are – as Shah puts it – “at the forefront of providing a more seamless physical and digital experience, with more value-adding services to their customers. A key unlock for them is access to the payment rails.”

Blockchain, not Crypto

As it is, peer-to-peer payments are widely used to enable informal and small business ventures, easing the logistics and cost of remittances. As the market globalises, there is an increased need for more efficient and lower-cost cross-border payments. The cryptocurrency ecosystem expanded by 2 300% between September 2019 and June 2021, particularly in developing countries, with Africa a notable early adopter. According to a policy brief released by the United Nations Conference on Trade and Development, significant proportions of Kenya’s (8.5%), South Africa’s (7.1%) and Nigeria’s (6.3%) populations are using digital currencies. In the digital assets market, the number of users in Africa is expected to reach 56.6 million by 2027. Worldwide, that forecasted number sits at 994 million.

In the last four years, eight African countries have launched initiatives to establish a central bank digital currency in their markets. South Africa has set up the Intergovernmental Fintech Working Group comprising regulators and market players to promote distributed ledger technology-driven (DLT-driven) innovation in financial markets.

The opportunity lies in the blockchain technology that underpins cryptocurrencies, rather than the cryptocurrencies themselves, to drive financial inclusion. Using blockchain to create “programmable money” can assist in eliminating fraud and human error in transactions, and improve transparency in financial records.

Blockchains can also provide mechanisms for fair and transparent microfinance and increased purchasing power to support the creation and growth of small enterprises that serve communities. Transparent social coordination tools afforded by blockchain-based organisational entities like decentralised autonomous organisations can empower small business collectives to gain access to competitive advantages like negotiating power to match larger businesses.

“Standard Bank remains at the forefront of research and development of blockchain and DLT in the African context,” says Standard Bank Head of Blockchain Ian Putter. “We are committed to the exploration of efficient digital payment rails and financial services that enable African commerce to flourish. This includes ongoing collaboration with major blockchain companies, like Algorand and Hedera. Improving the inclusion of the underserved is a core value of Standard Bank, and blockchain technology will no doubt provide an avenue for great impact on African markets in the coming years.”

Payment solutions that will succeed are those built not only by leveraging emerging technology but also through collaboration between traditional incumbent banks, regulators, MNOs, retailers and fintechs to solve the challenges that inhibit access to financial services in and outside Africa. The aim of collaborating is to create sustained economic growth and development in Africa. Empowering our partners by providing them with digital payments solutions is a key catalyst to accelerate the positive impact that this can ultimately create.

TEXT: Trevor Crighton

ccording to World Bank estimates, about 45% of 882 million adults in Africa do not have access to a bank account. There is no other market where the necessity to remove friction

and make financial services and payments more inclusive and accessible is more prevalent than on our own continent.

“If you consider adults who actively use their bank account, then this is likely to constitute a market of around 100 million adults across the continent,” says Sachin Shah, Head: Payments and Receivables, Transaction Banking at Standard Bank Corporate and Investment Banking. “But the moment you expand that to wallets, your target population grows to nearly a billion. That’s a massive leap.” Manufacturers and service providers want to be able to sell their products and services to these customers and unlock the growth potential which exists on the continent. Enabling payments to and from these customers is the catalyst through which this can happen.

Access to Payment Rails

South Africa is unique in the maturity of account payments and card-based solutions, which still form the primary means of payments processing and settlement in the market. The National Payment System Act in South Africa currently excludes non-banks from directly accessing the settlement system, which means that they require a bank sponsor to settle transactions.

This can be illustrated as a central hub of settlement participants radiating outwards to clearing participants, payment services, third-party payment providers and a final ring encapsulating customers, retailers and corporates. The picture looks like a target – and non-financial banking solutions providers will see it as exactly that. They’re currently only able to access the third-outermost ring that the third-party payment providers are regulated into, but they’re aiming for the bull’s-eye.

In most other markets, mobile or wallet payment volumes have overtaken account and card payments, especially as a form of settlement for low value, instant payment transactions. Whereas the principles in many instances are similar to South Africa’s National Payment System Act (78 of 1998), the models have also evolved based on local requirements. Banks including Standard Bank still play a critical role within this value chain – holding the trust accounts which contain 100% of the funds equivalent to the mobile money in circulation. This is the foundation of a partnership which can evolve to so much more.

“With every household in Africa expected to have access to a mobile phone with internet access by 2030 or even sooner, mobile wallets can provide more ubiquity than any other digital financial instrument,” says Shah. “The impact this can have on the digitisation of payments cannot be underestimated.” South Africa’s new interbank digital payment service PayShap is a step in that direction, enabling customers to pay and be paid instantly using a mobile phone number instead of having to share their bank account details.

The Face of Payments

“With the benefit of a vast subscriber base as well as a significant agent base, Mobile Network Operators (MNOs) are quickly becoming the face of payments across Africa” says Shah. “One of their key benefits is also being able to offer last mile access to cash – as cash transactions still constitute a significant percentage of all mobile money transactions”. Their growth potential has not gone unnoticed, with multi-million-dollar investments into the mobile money entities from global giants including Mastercard and Visa.

In South Africa, the retail sector, in turn, is also being rapidly disrupted. What started off as the provision of services like cashback at tills and bill payments is rapidly expanding to money remittances, the opening of bank accounts as well as strategies to offer their own wallets. Through their vast customer base and by leveraging the data that they hold, both the retailers and telcos are – as Shah puts it – “at the forefront of providing a more seamless physical and digital experience, with more value-adding services to their customers. A key unlock for them is access to the payment rails.”

Blockchain, not Crypto

As it is, peer-to-peer payments are widely used to enable informal and small business ventures, easing the logistics and cost of remittances. As the market globalises, there is an increased need for more efficient and lower-cost cross-border payments. The cryptocurrency ecosystem expanded by 2 300% between September 2019 and June 2021, particularly in developing countries, with Africa a notable early adopter. According to a policy brief released by the United Nations Conference on Trade and Development, significant proportions of Kenya’s (8.5%), South Africa’s (7.1%) and Nigeria’s (6.3%) populations are using digital currencies. In the digital assets market, the number of users in Africa is expected to reach 56.6 million by 2027. Worldwide, that forecasted number sits at 994 million.

In the last four years, eight African countries have launched initiatives to establish a central bank digital currency

in their markets. South Africa has set up the Intergovernmental Fintech Working Group comprising regulators and market players to promote distributed ledger technology-driven (DLT-driven) innovation in financial markets.

The opportunity lies in the blockchain technology that underpins cryptocurrencies, rather than the cryptocurrencies themselves, to drive financial inclusion. Using blockchain to create “programmable money” can assist in eliminating fraud and human error in transactions, and improve transparency in financial records.

Blockchains can also provide mechanisms for fair and transparent microfinance and increased purchasing power to support the creation and growth of small enterprises that serve communities. Transparent social coordination tools afforded by blockchain-based organisational entities like decentralised autonomous organisations can empower small business collectives to gain access to competitive advantages like negotiating power to match larger businesses.

“Standard Bank remains at the forefront of research and development of blockchain and DLT in the African context,” says Standard Bank Head of Blockchain Ian Putter. “We are committed to the exploration of efficient digital payment rails and financial services that enable African commerce to flourish. This includes ongoing collaboration with major blockchain companies, like Algorand and Hedera. Improving the inclusion of the underserved is a core value of Standard Bank, and blockchain technology will no doubt provide an avenue for great impact on African markets in the coming years.”

Payment solutions that will succeed are those built not only by leveraging emerging technology but also through collaboration between traditional incumbent banks, regulators, MNOs, retailers and fintechs to solve the challenges that inhibit access to financial services in and outside Africa. The aim of collaborating is to create sustained economic growth and development in Africa. Empowering our partners by providing them with digital payments solutions is a key catalyst to accelerate the positive impact that this can ultimately create.